Peabody Energy (BTU) reported its 4Q'12 financial performance today. BTU registered quarterly revenues of $2.01 billion, beating the analysts' estimates by $0.08 billion. I am bullish on the stock, as it has a superior gross margin figure of 28%, is currently trading at a cheap forward P/E of 10.9x, has higher ROE of 13% and ROA of 6% compared to its peers.

Peabody Energy is the largest private sector coal company, with customers in more than 25 countries. The company has operations in the U.S. and Australia. BTU fuels 10% of the U.S and 2% of the world's electricity generation by coal. BTU has annual revenues of $8.08 billion.

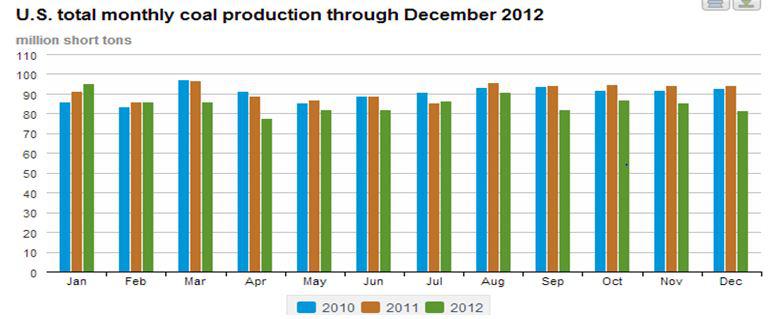

Industry Overview

The U.S coal industry had a tough last year, as a majority of the coal stocks lost significant amount of their market capitalization. The Market Vectors Coal ETF (KOL) was down approximately 20% in 2012, underperforming the broad market.

In 2012, U.S. coal fired electricity generation fell to 37.6%, a decline of 4.7% YoY. This decline was mainly due to decreasing natural gas prices that also led to a rise in the U.S. coal inventory level last year. However, to manage coal inventory levels, monthly coal production has been decreasing, which will support the coal prices going forward. The following chart shows declining monthly coal production from 2010 through 2012.

Graph 1

(click to enlarge)

Source: eia.gov

Financial Results

BTU reported 4Q'2012 revenues of $2.01 billion, beating the estimates by $0.08 billion. Adjusted earnings for the quarter were -$1.12, as compared to $0.98 in the same quarter prior year. The company sold 63.3 million tons of coal in the most recent quarter, down 7% YoY.

U.S. mining revenues for the company were $1.09 billion in 4Q 2012, down 5% YoY. On the other side, Australian mining revenues for the recent quarter were $0.9 billion, down from $0.925 billion in 4Q 2011. BTU reported adjusted EBITDA of $407 million for 4Q 2012, down from $584 million. However, BTU was able to reduce its selling and administrative expenses, which decreased by 50 bps YoY to 3.3% as a percentage of net sales.

Guidance

Given the tough times for the industry, BTU lowered its targeted CAPEX by 50% to $450-$550 million for 2013 compared to 2012. Also, in its recent quarterly earnings release, BTU guided for fiscal 1Q'13 losses in the range of 4 cents to 26 cents; wider than analysts' expectation of a 9 cent loss.

For 2013, BTU is expecting to register sales volumes of 230-250 million tons; including 180-190 million tons of U.S. sales, and 33-36 million tons of Australian sales.

For the full fiscal year 2013, analysts are expecting annual revenues of $8.09 billion and EPS of $0.76. Following are the analysts' EPS estimates from 2013 to 2015.

| | Dec 2013 | Dec 2014 | Dec 2015 |

| EPS Forecast | $1.01 | $2.38 | $4 |

Source: www.Nasdaq.com

Conclusion

I believe 2013 will be a better year for the U.S. coal industry compared to 2012 due to declining coal inventory level as shown in Graph 1 above. I am bullish on BTU and recommend investors buy the stock, as it has superior gross margins and a cheaper forward P/E compared to its competitors. The table below shows gross margins, ROE, ROA and forward P/E of BTU and its competitors.

| | BTU | Arch Coal Inc. (ACI) | CONSOL Energy Inc. (CNX) | Alpha Natural Resources, Inc. (ANR) |

| Gross Margin | 28% | 19% | 29% | 13% |

| ROE | 13% | - | 12% | - |

| ROA | 6% | 2% | 2.1% | - |

| Forward P/E (Based on 2014 EPS est.) | 10.9x | - | 14x | - |

Source: Yahoo Finance