There is an ongoing controversy on shale gas boom and bust. The controversy is whether shale gas is economical to produce. Critics say EURs (Estimated Ultimate Recovery) of shale wells were exaggerated using flawed models; and that the industry painted a rosy picture while the productions come out short of expectations.

Whether a shale gas well is economical or not relies on these things:

- The life cycle total costs of exploration and production.

- The EUR, estimated ultimate recovery from each well.

- How fast is the gas produced and turned into revenue?

- The market prices of natural gas produced.

I will discuss how the industry projects shale well declines; why the EURs are often over-estimated; and why the industry faces gloomy reality of non-profitability of shale gas wells. I will try to explain technical concepts using layman's English to investors. If you are confused, just look at the pictures and then go to the conclusions.

To B or not to B - That is the Question

I once wondered what the b parameter was. Arthur Berman mentioned it when he criticized the hyperbolic models that shale gas experts use to calculate EURs. Berman claimed that such models over-estimated EURs.

All natural gas (NG in brief) wells, conventional or shale gas, have highest daily production rates on day one. Production rates decline continuously throughout well life cycles. Shale gas wells could lose 80% of production rate in the first year. Thus modeling the declines correctly is the key to predict EURs. Since few shale wells have gone through whole life cycles, there is wigging room for experts to come up with different decline models.

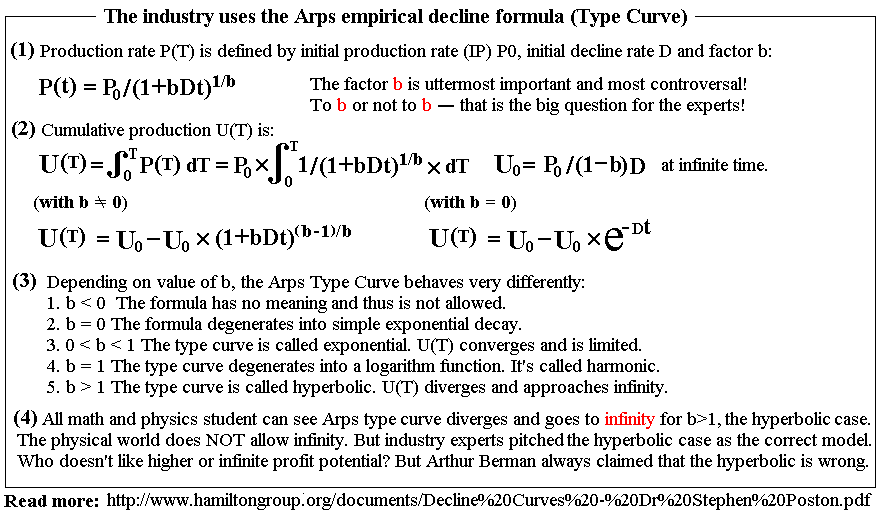

The NG industry uses a formula first developed by Arps, called type curve formula. It is an empirical formula. Empirical means there is no physics support, but by experience the formula seems to match actual data nicely. The Arps formula is describe as below:

(click to enlarge)

As it comes, 0

Not willing to point fingers, I believe there is a perfect explanation why they tend to come up with b>1. Read my detailed discussion. The Arps model has too few freely adjustable parameters to fit the data fully, so b is biased and could be off the accepted range.

But still, when b>1, the Arps type curve diverges to infinity. Thus it fails to model the long-term decline of gas wells correctly.

I had an alternative formula. But I will not elaborate here. I will use only the type curves that the industry uses for discussion here. The Marcellus shale type curve was found here.

Below are Arps type curves with various b parameters, compared with the Marcellus type curve:

(click to enlarge)

Arthur Berman pointed out that during early well productions; models with vastly different b values all look similar. The differences only show up in the long-term, leading to vastly different EUR values.

Since there is insufficient long-term data to verify models, let me assume the CHK model is correct to analyze Marcellus shale.

Profitability Case Study on Marcellus Shale

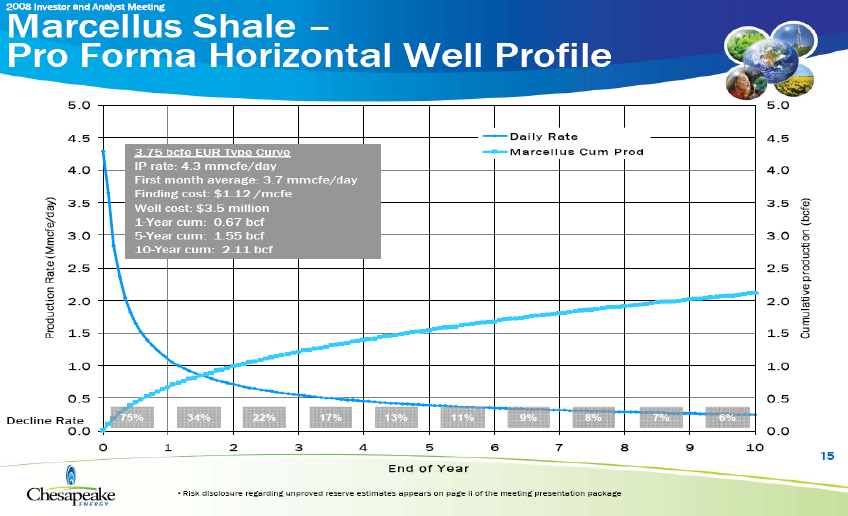

The CHK Marcellus type curve chart contains parameters that I could to re-construct the data model for calculation:

(click to enlarge)

The D and b parameters were not given. But given the cumulative production at one, five and ten years, I easily found out the D and b used, and verified that I had the correct values:

- D = 1/3 per month; b = 1.461 (b>1!); IP = 4.11 MCF/day. I obtained the same 1-year, 5-year and 10-year productions.

It came out that the claimed EUR of 3.75 BCF was the cumulative production after exactly 500 months. The daily production would drop to 0.095 MCF/day by then, or worth $228 at $2.40/mmBtu gas price, enough to pay one day's minimum wage.

Did Chesapeake Energy (CHK) honestly believe that shale gas wells could last that long and at such a low yield? In fact, as the function is divergent (b = 1.461 > 1), they could theoretically keep the wells running forever and brag about any high EUR number they like.

In mathematics, Arps curves with large b, especially those with b>1, have terminal declines that approach zero. Limited natural resources should have none zero terminal declines. As they are depleted, the volume that comes out is roughly proportional to what remains. In math, when the change rate of a quantity is proportional to the quantity that remains, it is known to be an exponential decline.

We can disputes the decline models another time. Using the existing CHK models, I can calculate the profitability of Marcellus shale based on different gas prices and costs.

Gloomy Profitability Reality of the Marcellus Shale Wells

The industry produces shale gas to make money, not to provide a charity. Currently natural gas prices are deeply non-profitable. Most believe that the NG prices will recover. The question is, once the gas prices return to normal levels, say $4/mmBtu, will the shale gas industry be able to make a profit?

Let me put away the shenanigans in creative financial bookkeeping and cost accounting when it comes to profitability. Let me define profitability as there is enough profit potential in the sector that a reasonable investor would feel inclined to spend his own money to explore and produce shale gas.

When you are playing with your own money, not other people's money, you are forced to be honest with all related costs.

Some NG executives claimed they were profitable even at $2 gas prices. They probably did not count costs like land leasing, G&A expenses, and interests on loans. They probably expected to produce the wells for 40 or 50 years. (CHK used 500 months life span to obtain 3.75 BCF EUR for Marcellus wells). They might not have calculated inflation and depreciation of currency. I want to use data to find out.

Spending $15M to drill a well and break even in 30 or 50 years is not a business proposition you want to go home to tell your mom about. There should be a reasonable hope that when all dollars and cents are counted, you recover all the costs reasonably soon, and then you begin to make a reasonable profit.

Let's start with lifetime total costs of Marcellus wells. CHK gave $3.5M drilling cost, $1.12/mmBtu finding cost for a EUR of 3.75 BCF. That makes $7.7M. The actual figures are higher when you count in all the excluded costs. The figures were provided several years ago. Consider how much gold and other commodities have gone up, it is safe to say the costs are proportionally higher today.

I think a lifetime per well cost of $15M is reasonable for calculation. There are also interest costs. Let's say the interest rate is 5%.

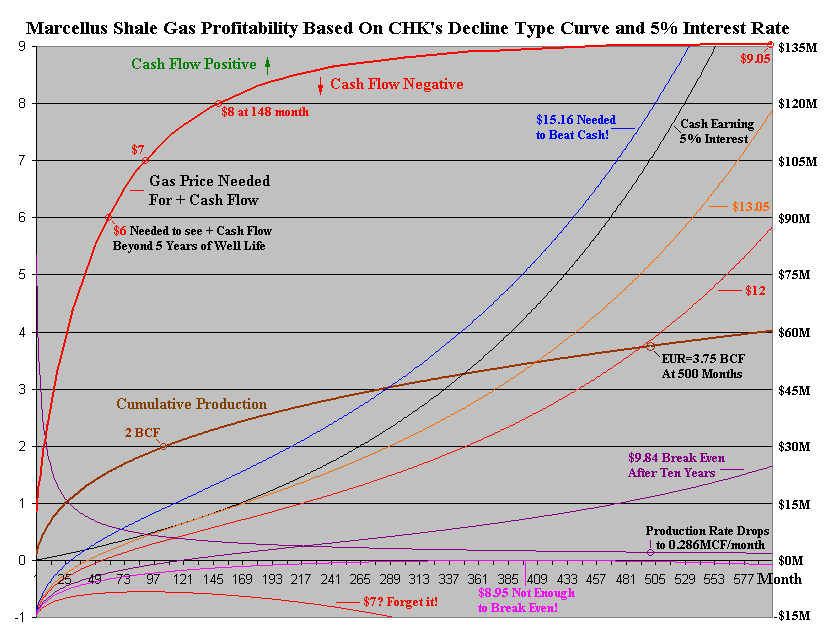

Maintaining production and delivering the gas also has costs. I will assume $30K per month for that. My profitability model starts with $15M in debt. As gas revenue comes in, the debt is gradually paid off. Where the lines cross the X-axis are the break-even points.

Here are the results. I added a black line representing $15M cash that bears 5% interest for a comparison:

(click to enlarge)

The result is pretty distressful. Pay attention to the thick red line. It indicates the minimum gas price needed for positive cash flows at any given time in a well's life.

The upper left side of the curve is the cash flow positive region. It means you generate enough flow of sales revenue to pay off debts. Below and to the right is the cash flow negative region, meaning you have to continuously borrow more debts to stay in business.

For example, at 5 years, or 60 months, the cash flow positive gas price is at $6. At that price, the wells less than 5 years old will see positive cash flow. The producers operating wells older than 5 years will keep burning cash.

The picture is gloomy even based on CHK's own production model:

- Forget about $7 gas price. It is a shame to even mention it.

- At $8.95 you could see the light of hope after paying off the debts after 33 years. But the production decline took things down hill before you see a dime of profit.

- $9.84 allows you to break even in just ten years. The profits are all yours after that, although it is not much. You would have made $25M profits after 50 years. A big part of that profit came from the 5% interest your accumulated profits earned from banks.

- $12 does not look bad. But the guy who earned 5% interest on his cash deposit did better. If gas price was at $13.05 you could almost beat him at one point.

- At $15.16, we are finally talking about some profits. You paid off the debts in 30 months. You beat the cash guy in 3.5 years. But you were not getting rich quick! In 41 years, the cash guy reached $100M. You were ahead by just $12.7M. What a shame!

I am not calling for bank deposits. I call for investments in things that make sense and make profits. Having seen above numbers, are you inclined to tell mom to take money out of your bank account to buy assets from CHK to drill for gas? I bet not.

The Reality Could Be Worse Than the Above Projections

The projections were bad enough. But the reality could be worse! The discussions above were based on a model that the industry provided. The model probably exaggerated the EUR and under-estimated the steep decline of gas wells. The real data could portrait a gloomier picture.

Making matters worse is NG producers have racked up mountains of debts developing shale gas wells. The shale gas over-drilling, over production, the decade low NG prices and the subsequent capital destruction is destroying the US NG industry.

America still needs natural gas. The NG industry as a sector will not go away. But there are serious questions on whether shale gas is really a viable energy source, or is hydraulic fracturing technology really effective in the long-term. People have too many questions, but the industry refused to tell the full truth. Even today, there is still no disclosure on what is contained in the hydraulic fluid used.

Do you feel comfortable investing in a sector where you do not know the full truth? I don't.

The Implication for Investors

In recently times we heard a lot of talks of abundant, cheap and clean natural gas to replacing dirty and filthy coal. Coal is dirty. But we do not have a choice. Coal is still the cheapest and most abundant fossil fuel we can count on. Old king coal is not going away any time soon. I am convinced the deeply discounted coal sector is the best investment opportunity in 2012.

I am bullish in natural gas prices. But I do not recommend United States Natural Gas (UNG) or any ETF based paper future contracts. Stay tuned! I plan to write about the collapse of the NG long tail production. I will tell you what I mean in my next article.

I continue to caution people to pay attention to the unfolding drama of capital destruction in the natural gas sector. A lot of shale gas players need to go belly up. There will be a time when all the nasty stuffs are put out for all to see. At that time there might be some survivors worth picking up. But avoid these names now:

- Chesapeake Energy Corp. [CHK]

- Constellation Energy (CEP)

- Cabot Oil & Gas Corp. (COG)

- ConocoPhillips (COP)

- Anadarko Petroleum Corp. (APC)

- EOG Resources Inc (EOG)

- Devon Energy Corp. (DVN)

- Baker Hughes Inc. (BHI)

- Southwestern Energy Co. (SWN)

- Sand Ridge Energy (SD)

- Pioneer Natural Resources (PXD)

- Magnum Hunter Resources (MHR)

- Kinder Morgan Energy Partners (KMP)

- Enerplus Resource Fund (ERF)

- Carrizo Oil & Gas (CRZO)

- Callon Petroleum (CPE)

- Enterprise Products Partners LP (EPD)

- Goodrich Petroleum (GDP)

- GMX Resources (GMXR)

- IDT Corp (IDT)

- Lucas Energy (LEI)

- Rex Energy (REXX)

- Approach Resources (AREX)

- Natural Gas Services Group (NGS)

- Breitburn Energy Partners (BBEP)

- National Fuel Gas (NFG)

- Range Energy Resources (RRC)

- Petroquest Energy (PQ)

- Unit Corp. (UNT)